Was FTX A Ponzi Scheme From The Beginning?

What we know:

- In January 2018, just five months after launching, Alameda Research took a massive loan. The loan totaled $117M, and carried an annual interest rate of 43%. Officially, they needed the loan for doing Kimchi arbitrage - however, it was dubious that they ever did any arbitrage.

- In January 2018, Alameda also raised funds from Redline Blockchain Capital - a shady Chinese company that described itself as an "encrypted venture capital institution", and whose CEO is connected to 92 different companies.

- During the first few months of 2018, Alameda lost track of millions of dollars. They also mistakenly recorded losses as profits, and vaporized money on simple cryptocurrency transfer mistakes.

- In March 2018, things had gotten so bad that the people who lent Alameda money (Jaan Taallinn and Luke Ding) recalled the majority of their loan, and demanded that the recalled part should be paid back immediately, with interest.

- In April 2018, half of Alameda's employees quit, due to "concerns over risk management and business ethics".

- Later that year, FTX was founded.

- During the first half of 2019, FTX received a large amount of customer deposits. While we do not know the exact value of these deposits, they were large enough to facilitate a daily trading volume of $50M.

- In August 2019, FTX completed its first seed round, raising $8M from 5 different venture capital firms.

- Later that year, Alameda paid back the remainder of its loan, and bought back the shares owned by Redline Blockchain Capital.

While there is no conclusive evidence yet, the events that took place during the first half of 2018 suggest that Alameda/FTX might have been a Ponzi scheme from the very beginning.

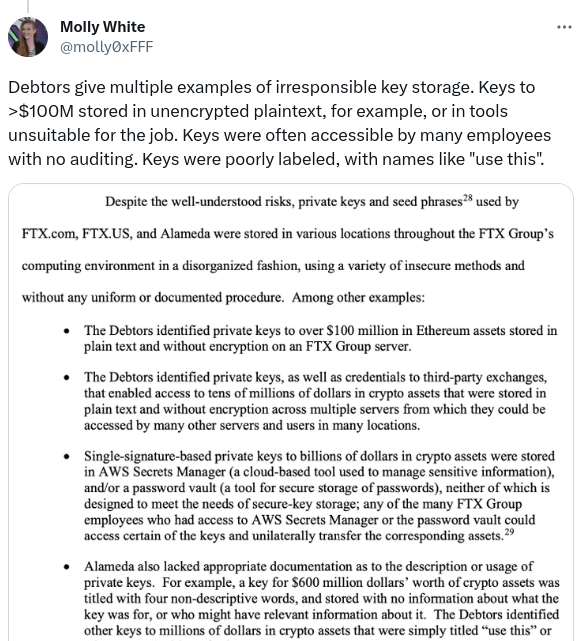

$20M hole in Alameda's balance sheet

Alameda's loan carried a monthly interest of $4.2M. When you combine this with the millions that Alameda lost on basic transfer mistakes and lack of accounting, it is not hard to see why FTX had to be created.

The Kimchi arbitrage trading, while profitable, was likely just a smokescreen, to keep investors and creditors complacent. There’s no evidence to suggest that SBF ever took advantage of the Kimchi premium. Doing so required special relationships with local banks, that not even established hedge funds and proprietary trading firms were able to establish.

By the end of 2018, in lieu of any profits from arbitrage, Alameda would have had racked up a considerable hole in its balance sheet. Based on the size of the interest payments and the millions lost on basic operational mistakes, we can estimate this hole to be at least $20M.

With cash reserves almost depleted, and massive debt, SBF was faced with two choices: Declare Alameda bankrupt, or try to raise more money, and pay off existing creditors/investors with that money (aka run a Ponzi scheme).

If SBF was to be successful at the latter, it is clear that he needed to do something different. Alameda was a failure - nobody, not even loan sharks, were willing to lend them any money.

FTX

One of the most popular ways to run a Ponzi scheme is to run a cryptocurrency exchange. You create a steady inflow of cash (customer deposits). This inflow of cash typically outpaces your outflow of cash (customer withdrawals).

Since you also act as custodian, you have full control of the customer deposits, and can spend some of them on growing your Ponzi scheme (acquiring additional suckers).

It is unknown how many cryptocurrency exchanges currently function as Ponzi schemes. However, there are likely a fair amount of them out there. After all, cryptocurrency exchanges that are Ponzi schemes have a unique competitive advantage: A large part of their customer deposits can be spent on marketing, allowing them to grow faster than legitimate exchanges.

Like most other successful cryptocurrency exchanges, FTX had a positive net flow during its first year of operation. It is not far-fetched to assume that many of the deposits on FTX were transferred directly to Alameda, and used to pay off Alameda's debt. With $50M in customer deposits, and $8M in seed money, it would have been possible for Alameda to pay back the remainder of its high interest loan - and settle all of the outstanding interest.

Was FTX always a Ponzi scheme?

Even if the Alameda/FTX constellation was initially run like a Ponzi scheme, it is not clear whether it always had a hole in its balance sheet. It is possible that the constellation was initially insolvent, but became solvent some time during 2020 or 2021. After all, successful cryptocurrency exchanges make a ridiculous amount of money from trading fees - and FTX was no exception.

Bitfinex is one example of a cryptocurrency exchange that once had a significant hole in its balance sheet, but later managed to become solvent again, thanks to the trading fees it earned (and some clever bankruptcy engineering around its BFX token).

What we know for sure is that Alameda/FTX had a huge amount of expenses during the first half of 2018, and (presumably) very little income. The company lost millions on basic operational mistakes - something that can be excused, if you are making tens of millions from arbitrage - but given the amount of internal conflict, it is unlikely that the Kimchi arbitrage story was ever the success that it was purported to be.